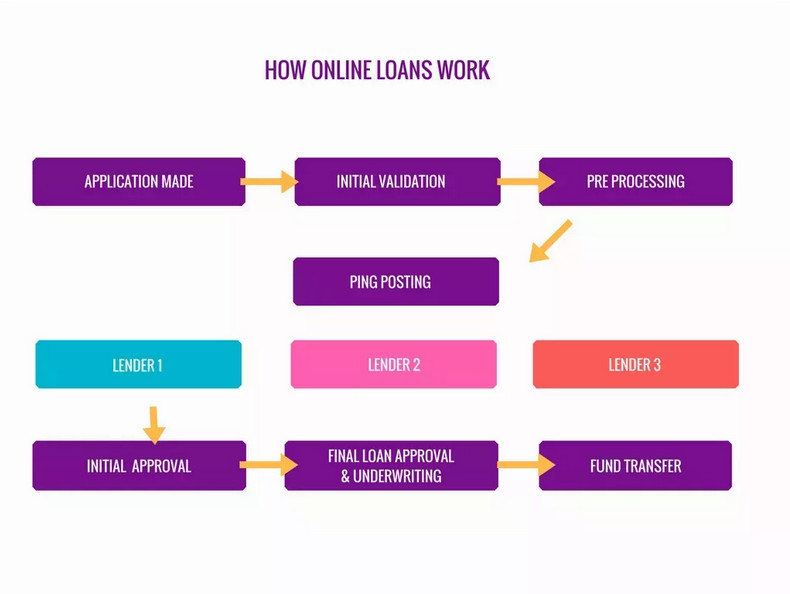

A credit broker ( Flexfinans partner with Myloan.co.za ) is a financial intermediary or agent that connects borrowers with potential lenders. Credit brokers do not provide loans directly; instead, they facilitate the loan application process by matching borrowers with suitable lenders based on the borrower’s financial profile and loan requirements. Here’s how credit brokers work and the key differences between a credit broker and a direct lender:

Credit Broker:

- Matching Service: Credit brokers act as intermediaries between borrowers and lenders. They have a network of lenders with whom they work.

- Loan Options: A credit broker helps borrowers find loan options by collecting information about the borrower’s financial situation, credit history, and loan needs.

- Comparison: Brokers often present borrowers with loan offers from multiple lenders, allowing them to compare interest rates, terms, and conditions.

- Access to Multiple Lenders: Credit brokers may have access to a wide range of lenders, including banks, credit unions, online lenders, and other financial institutions.

- Application Assistance: Brokers can assist borrowers in completing loan applications and gathering the necessary documentation.

- Fee Structure: Credit brokers may charge a fee for their services, either to the borrower, the lender, or both.

Direct Lender:

- Loan Provider: Direct lenders are financial institutions that provide loans directly to borrowers. When you borrow from a direct lender, you are dealing directly with the entity that will fund your loan.

- Limited Loan Options: Direct lenders offer their own loan products, and you have access only to the loans they provide.

- Underwriting and Approval: Direct lenders handle the underwriting and approval process, determining whether you qualify for a loan based on their specific criteria.

- Interest Rates and Terms: The interest rates, terms, and conditions of the loan are determined by the direct lender.

- No Broker Fees: Borrowing from a direct lender typically does not involve paying fees to an intermediary.

Choosing between a credit broker and a direct lender depends on your preferences, financial situation, and loan needs. Credit brokers can be valuable for borrowers who want to compare multiple loan offers or who have a challenging credit history. However, it’s essential to carefully review any fees associated with using a broker.

On the other hand, direct lenders are appropriate when you prefer a more straightforward borrowing process, have a clear understanding of the loan you need, and are comfortable working directly with a single lender.

Regardless of whether you choose to work with a credit broker or a direct lender, it’s crucial to thoroughly understand the terms and conditions of the loan and ensure that the loan aligns with your financial goals and capacity for repayment.

Compare Loans in South Africa

Comparing loans in South Africa involves assessing various factors to determine which loan product is the most suitable for your financial needs and circumstances. Here’s how to effectively compare loans:

- Loan Type:

- Determine the type of loan you need, such as a personal loan, home loan, car loan, or payday loan, based on your specific requirements.

- Interest Rates:

- Compare the interest rates offered by different lenders. Pay attention to whether the interest rate is fixed or variable.

- Keep in mind that the Annual Percentage Rate (APR) provides a more comprehensive view of the loan’s cost, as it includes all associated fees.

- Loan Amount:

- Assess the minimum and maximum loan amounts offered by various lenders to ensure they meet your borrowing needs.

- Loan Term:

- Evaluate the loan term options available. Longer loan terms typically result in lower monthly payments but may lead to higher overall interest costs.

- Fees:

- Examine the fees associated with the loan, such as origination fees, application fees, early repayment penalties, and monthly service fees.

- Repayment Schedule:

- Consider the loan’s repayment schedule, including the frequency of payments (monthly, weekly) and the available methods (debit order, bank transfer).

- Credit Requirements:

- Understand the credit score and financial criteria required to qualify for the loan. Some loans are accessible to borrowers with lower credit scores, while others require a higher creditworthiness.

- Additional Features:

- Some loans may offer additional features, such as the option to skip a payment, make extra payments, or access a redraw facility (for home loans).

- Security or Collateral:

- Determine whether the loan is secured (requires collateral, like a home or car) or unsecured (no collateral needed).

- Loan Approval Time:

- Compare the time it takes for loan approval and disbursement. Some lenders offer quick approval and funding, while others may have a more extended application process.

- Customer Service:

- Research and read reviews to assess the quality of customer service and responsiveness of the lender.

- Early Repayment Options:

- Determine whether there are any penalties or restrictions on making early repayments. Some loans may charge penalties for paying off the loan ahead of schedule.

- Repayment Insurance:

- Inquire about the availability of repayment insurance or credit life insurance to protect yourself in case of unforeseen circumstances.

- Loan Amount and Interest Rate Variations:

- Request quotes from multiple lenders to compare their loan offers side by side. This allows you to choose the most favorable terms.

- Overall Cost:

- Calculate the total cost of the loan over its duration to assess the financial impact and affordability.

When comparing loans, it’s essential to consider your financial situation, needs, and long-term financial goals. Ensure that the loan you choose aligns with your budget and your ability to repay it responsibly. Be thorough in reviewing the loan terms and conditions, and do not hesitate to seek clarification from the lender if you have questions.